Thực hiện free test

[SUMMARIES]

New EP applications must meet the S$6,000 threshold and S Pass candidates must earn at least S$3,600 starting January 1, 2027, with renewals following on January 1, 2028.

Meeting the minimum salary no longer guarantees approval as the COMPASS C1 criteria mandates your payroll align with the 65th percentile of local PMET wages in your sector.

Failing to recalibrate salaries for key personnel earning near old thresholds will trigger a “talent vacuum” through renewal rejections in 2028, causing severe operational paralysis.

Enterprises with constrained budgets should optimize non-salary COMPASS pillars, such as nationality diversity and local hiring, to secure necessary approval points.

Businesses can leverage the Job Redesign+ grant to receive up to 70% government funding, capped at S$150,000, to boost productivity and offset these mandatory salary hikes.

[/SUMMARIES]

With the Ministry of Manpower (MOM) officially raising the bar for Employment Pass (EP) and S Pass salaries starting in 2027, businesses face a new set of compliance and financial challenges. This update breaks down the essential figures and timelines you need to know to protect your workforce and sustain your growth in a higher-productivity economy.

On March 3, 2026, MOM announced increased salary benchmarks to maintain the quality of the foreign workforce. To achieve this, the Ministry has mandated new minimum qualifying salary hikes. These figures serve as the baseline “floor” for eligibility, with higher thresholds applicable to older candidates and those in the Financial Services sector:

| Pass Type | Current Minimum Salary | New Minimum Salary (From 2027) |

|---|---|---|

| Employment Pass (EP) | S$5,600 | S$6,000 |

| S Pass | S$3,300 | S$3,600 |

Proactive Insight: Enterprises should brace for a long-term upward trajectory; the S Pass threshold is projected to reach S$4,000 – S$4,500 by 2030.

MOM has provided a dual-phase “runway” to allow businesses sufficient time for financial and manpower restructuring. Compliance will be assessed based on the following milestones:

This structured implementation means that while new hires will be affected immediately in 2027, companies have an additional year to evaluate and adjust salaries for existing pass holders before their 2028 renewals.

For Singapore enterprises, the 2027-2028 salary hike is not a localized payroll issue; it is a fundamental shift in business cost structures.

Elevating the salary floor to S$6,000 (EP) and S$3,600 (S Pass) directly inflates fixed overheads. For SMEs, these mandatory adjustments can erode projected profit margins if not integrated into 2027-2028 fiscal planning. Furthermore, businesses must navigate the “wage-push” effect: raising salaries for foreign professionals often triggers a ripple effect, necessitating upward adjustments for local staff to maintain internal pay equity.

Under the Complementarity Assessment Framework (COMPASS), meeting the minimum salary is no longer enough. Criterion 1 (C1) benchmarks an applicant’s salary against the 65th percentile of local PMET wages within your specific sector. As the baseline rises, the “market median” shifts. Firms that fail to proactively recalibrate compensation packages risk scoring zero on the C1 pillar, leading to pass rejections even if they technically meet the S$6,000 threshold.

The 2028 renewal window represents a critical “talent cliff.” High-value employees currently earning near the current thresholds may suddenly become ineligible for renewal. Losing institutional knowledge and specialized expertise due to a compliance oversight is a strategic failure that can stall long-term projects and weaken market position.

In Singapore’s meritocratic labor market, a work pass rejection is a threat to operational continuity. A rejected renewal often grants the holder only a short stay (typically 30 days) to exit the country, creating a “talent vacuum” characterized by:

Preparation is the definitive defense against regulatory shifts. To maintain compliance and operational stability, Koobiz recommends the following strategic steps:

The first phase involves a deep-dive review of your current foreign talent pool. Proactivity is key to preventing a “talent cliff” in 2028.

While Salary (C1) is a primary factor, the COMPASS framework offers multiple pathways to success. If drastic salary hikes are not commercially viable, you must strengthen other pillars to secure the necessary points:

[CTA]

TITLE: Need help navigating Singapore’s import requirements? It’s good!

[/CTA]

Rather than simply inflating payroll, look for strategic ways to restructure compensation and productivity.

At Koobiz, we understand that these regulatory shifts are more than just figures on a spreadsheet, they are pivotal milestones for your company’s growth and stability in Singapore. As the 2027-2028 deadlines approach, leaving your compliance to chance is a risk your business should not have to take.

Our integrated approach serves as a comprehensive “Compliance Shield” for your enterprise:

Don’t let the 2027-2028 changes catch you off guard. Secure your operational continuity and talent pipeline today. Contact Koobiz now for a 360° Workforce Health Audit. Let us transform these regulatory challenges into your competitive advantage.

[SUMMARIES]

From March 2026, the EWTP (WDG(JR+)) replaces PSG-JR, boosting total grant support from S$30,000 to S$150,000 for AI and job redesign.

Support is split into Three Funding Pillars: Consultancy (S$50k), Capability Building (S$60k), and Tech Solutions (S$90k) to ensure a complete business transformation.

Starting late 2026, the S$10,000 SFEC credit becomes an “Online Wallet,” allowing eligible firms to offset costs immediately instead of waiting for reimbursements.

To qualify, companies must be Singapore-registered, maintain at least 3 local employees (SC/PR), and stay in “Good Standing” with ACRA.

The formation of Workforce and Skills Singapore (WSSG) signals more stringent auditing on the Business Grants Portal (BGP), requiring technically precise KPIs and documentation.

[/SUMMARIES]

Is your business ready for the AI revolution? The Ministry of Manpower (MOM) has just introduced the S$400 million Enterprise Workforce Transformation Package (EWTP), a game-changer for Singapore enterprises. This isn’t just a grant; it’s a powerful opportunity to modernise your workforce with up to 70% funding support, capped at S$150,000 per company. At Koobiz, we’re here to help you navigate this transition smoothly.

During the recent 2026 Committee of Supply Debate, a new roadmap was unveiled to help local businesses thrive. The EWTP represents a strategic shift by the government, moving away from fragmented subsidies to a unified framework that supports your evolution. Whether you are facing a tight labor market or looking to integrate AI, this initiative is designed to help you rethink your workforce and emerge stronger in a high-tech landscape.

EWTP stands for the Enterprise Workforce Transformation Package. Think of it as a “super-package” created by MOM to consolidate multiple support schemes into one place, making it easier for your business to grow.

Starting March 2026, the star of this package, the SkillsFuture Workforce Development Grant (Job Redesign+), or WDG(JR+) will officially take center stage. For business owners, this is exciting news: the funding ceiling is jumping from a modest S$30,000 under the old PSG-JR program to a robust S$150,000 per enterprise.

Here is how the S$150,000 support is broken down for your business:

Note on Funding: While your company can flexibly combine these components to suit your goals, please note that the total overall support for each enterprise is capped at S$150,000.

Bonus for Cash Flow: From late 2026, the SkillsFuture Enterprise Credit (SFEC), a S$10,000 credit will act as an “Online Wallet.” This allows you to immediately offset out-of-pocket costs instead of waiting months for reimbursements. To qualify, you simply need to be a Singapore-registered entity with at least three local employees.

While the EWTP presents a golden opportunity, navigating this transition without a professional roadmap can expose your business to unforeseen vulnerabilities. In an era where Singapore is raising the bar for corporate governance, a “DIY” approach to transformation often leads to costly setbacks.

The most immediate challenge is the escalating cost of operations. From January 1, 2027, the minimum qualifying salary for Employment Pass (EP) holders will rise to S$6,000, while the S Pass threshold increases to S$3,600 (projected to reach S$4,500 by 2030). Combined with the 1.5% to 1% increase in CPF contribution rates for senior workers, the financial pressure is real. Without securing the EWTP’s S$150,000 support, your company must bear 100% of the costs for AI integration – a heavy strain on any financial reserves.

Applying for government grants is much more than just filling out a form; it is about telling a compelling story of why your business deserves support. With the launch of the new Workforce and Skills Singapore (WSSG), the vetting process is becoming more synchronized and detailed. We often see great projects miss out on funding not because the idea wasn’t good, but simply because internal documents like Board Resolutions or Impact Reports didn’t quite hit the technical marks required by the Business Grants Portal (BGP)..

Compliance is the non-negotiable foundation of doing business in Singapore. MOM prioritizes grants for companies in “Good Standing.” If your entity has been negligent in statutory filings, such as late Annual Returns or inaccurate ACRA records, you risk immediate disqualification from the EWTP. Furthermore, as the Local Qualifying Salary (LQS) rises to S$1,800 in July 2026, any administrative oversight could lead to work pass freezes or a “blacklist” status for future incentives.

Finally, there is the risk of strategic obsolescence. While your competitors leverage the S$90,000 Workforce Tech Solutions sub-cap to automate tasks and optimize talent through AI, staying stagnant creates a widening productivity gap. In Singapore’s hyper-competitive market, falling behind in technology adoption doesn’t just mean lower efficiency – it means losing your edge in an increasingly automated world.

[CTA]

[/CTA]

To successfully unlock the S$150,000 EWTP support, your enterprise must move beyond “intention” and focus on “implementation readiness.” The following three steps are critical to ensuring your application is not just submitted, but approved.

At Koobiz, we understand that successful transformation begins with a solid foundation. Whether you are a newly established startup or an expanding enterprise, your ability to access the S$150,000 EWTP support depends entirely on your legal and administrative readiness.

Secure your future in an AI-driven economy with a partner that understands the rules of success in Singapore. Contact Koobiz Today for a comprehensive compliance audit and start your journey toward being “Grant-Ready”!

[SUMMARIES]

All GST-registered businesses must adopt InvoiceNow for direct IRAS submissions through a phased rollout from Nov 2025 to Apr 2031.

Post-deadline, invoices not transmitted via the Peppol network will be deemed invalid, leading to the rejection of GST input tax claims.

Digital integration enables IRAS to perform instant cross-verification between buyers and sellers, flagging discrepancies immediately instead of during year-end audits.

Early adopters can secure government grants of up to S$1,000 for SMEs and S$5,000 for larger firms, including free software for smaller enterprises.

Adoption of the Peppol standard allows your business to seamlessly integrate with international jurisdictions using similar e-invoicing systems, such as the EU, Australia, and Japan.

[/SUMMARIES]

Following the COS Debate 2026, the Singapore Government is mandating InvoiceNow for all GST-registered businesses to automate tax submissions to IRAS. This shift replaces manual processing with digital efficiency, accelerating payment cycles and streamlining compliance for over 90,000 firms.

The GST InvoiceNow Requirement is being phased progressively to allow businesses-from SMEs to MNCs-adequate lead time to align their IT refresh cycles with these new compliance standards.

| Effective Date | Affected Taxable Entities |

|---|---|

| 1 Nov 2025 | Newly incorporated companies opting for voluntary GST registration. |

| 1 Apr 2026 | All new voluntary GST registrants, irrespective of incorporation date or legal structure. |

| 1 Apr 2028 | All new compulsory GST-registrants AND existing GST-registered businesses with annual supplies <= S$200,000. |

| 1 Apr 2029 | Existing GST-registered businesses with annual taxable turnover <= S$1 million. |

| 1 Apr 2030 | Existing GST-registered businesses with annual taxable turnover <= S$4 million. |

| 1 Apr 2031 | All remaining GST-registered businesses (Annual supplies > S$4 million). |

Managed by the Infocomm Media Development Authority (IMDA), InvoiceNow is Singapore’s nationwide e-invoicing network based on the international Peppol standard.

Unlike legacy methods such as transmitting PDF invoices via email which still necessitate manual data entry, InvoiceNow facilitates the direct exchange of structured digital data between disparate accounting systems. For your organization, this ensures that upon invoice issuance, data is transmitted instantaneously to both the counterparty and IRAS, effectively eliminating human error and accelerating GST audit and refund processes.

In Singapore’s evolving landscape, tax compliance is shifting toward real-time transparency. Adopting InvoiceNow is no longer optional; it is a statutory mandate essential for maintaining your company’s standing with IRAS.

Direct data transmission provides IRAS with instantaneous transaction visibility. This enables automated cross-verification between buyers and sellers. Any discrepancies that previously surfaced only during periodic audits will now be flagged immediately, significantly increasing the likelihood of targeted queries for inconsistent data.

The most critical financial risk lies in your GST input tax claims. Beyond the deadlines, invoices not sent via InvoiceNow may be deemed invalid for GST purposes. This could lead to the rejection of tax credits, directly inflating your liabilities and straining your corporate cash flow.

While grants of up to S$1,000 for SMEs and S$5,000 for larger firms are available, the “cost of delay” is substantial. Waiting until 2031 risks rushed integration, premium vendor rates due to surging demand, and potential operational downtime during the mandatory switch-over.

To navigate the 2031 mandate effectively, businesses must move beyond reactive compliance. Taking proactive steps now allows you to leverage government support while optimizing your internal financial infrastructure.

The priority is verifying if your current accounting or ERP solution is “InvoiceNow-ready.” Consult the IMDA-accredited IRSP list to confirm compatibility. If you utilize an in-house enterprise solution, you must engage an accredited Access Point Provider (AP) to establish a secure connection to the Peppol network. Ensuring your software can transmit structured data directly to IRAS is the cornerstone of the new GST requirement.

The Singapore government is incentivizing early movers with significant financial support. SMEs can access InvoiceNow-Ready Solutions for free until March 2031 and may be eligible for a new grant of up to S$1,000 to defray operational costs. Larger businesses adopting the system ahead of their 2031 deadline can receive a grant of up to S$5,000. Beyond financial incentives, early adoption allows your team to refine digital workflows in a low-pressure environment, ensuring seamless GST filing long before it becomes mandatory.

The transition to InvoiceNow is the perfect opportunity to eliminate manual bottlenecks. By digitalizing your bookkeeping, you automate the reconciliation of purchase and sales invoices. This reduces human error, shortens payment cycles, and positions your business to integrate globally with jurisdictions using similar e-invoicing standards, such as the EU, Australia, and Japan.

Navigating the 2031 InvoiceNow mandate requires more than just new software; it demands a robust digital accounting strategy. At Koobiz, we provide end-to-end Accounting & Bookkeeping services specifically engineered to align with Singapore’s evolving tax landscape.

Don’t wait for the mandatory deadline. Contact Koobiz today for a Compliance Health Check and secure a seamless digital future for your enterprise.

[SUMMARIES]

Starting mid-March 2026, IRAS will issue Direct NOAs to 1 million taxpayers based on employer-submitted AIS data.

Automated billing means any clerical error in your payroll is instantly exposed to employees and tax authorities, triggering immediate audits.

April 18, 2026, is the final cutoff for all tax filings and adjustments; missing this leads to severe statutory penalties.

Inaccurate reporting carries heavy financial penalties and places personal legal accountability on both Directors and Company Secretaries.

Secure your business by auditing Form IR8A/Appendix 8A now and transitioning to monthly digital bookkeeping with Koobiz.

[/SUMMARIES]

The YA 2026 tax season marks a significant milestone in Singapore’s digital tax transformation. While promising a seamless experience for individuals, this shift introduces a new level of transparency and regulatory scrutiny for employers. As the Inland Revenue Authority of Singapore (IRAS) takes the lead in issuing direct bills, the accuracy of your corporate data submission now sits at the very heart of tax compliance.

Starting from mid-March 2026, IRAS will issue direct tax bills-officially known as the Direct Notice of Assessment (Direct NOA) to approximately 1 million taxpayers. This initiative is a major expansion of the No-Filing Service (NFS), designed to automate the tax process for a significant portion of the workforce.

Under this mechanism, eligible taxpayers receive their finalized tax bills directly without having to file a manual return. IRAS calculates these tax liabilities using data-driven automation, transitioning from a “self-declaration” model to a proactive “direct assessment” model.

The integrity of these direct bills relies entirely on third-party data. For most employees, the “source of truth” is the Auto-Inclusion Scheme (AIS). Consequently, the figures appearing on an employee’s tax bill are a direct reflection of the salary, bonus, and benefits-in-kind submitted by your company to the myTax Portal.

For employees, direct billing is a seamless upgrade. For business owners, however, it functions as a “Visibility Trap.” Because IRAS now leverages your corporate data to bill individuals directly, reporting errors are no longer buried in paperwork – they are delivered straight to your employees’ mobile devices, creating an immediate feedback loop with the tax authorities.

With 1 million taxpayers receiving their NOAs, every dollar will be scrutinized. If an employee’s tax bill is inflated due to a clerical error in your AIS submission or Form IR8A, they will likely file an immediate objection. In this digital era, a “Data Mismatch” is a high-priority red flag. An employee dispute can trigger IRAS’s automated systems to cross-verify your company’s internal ledgers, often escalating into a comprehensive corporate audit.

Incorrect filings do more than just invite regulatory heat; they erode your internal corporate culture. Discrepancies lead to employee frustration and a loss of trust in management. In Singapore’s competitive talent landscape, being perceived as a firm that “fails at payroll” is a significant reputational liability that can hamper recruitment and retention.

Under the Singapore Income Tax Act, the legal onus for accurate reporting rests squarely on the company’s leadership. IRAS maintains a stringent stance on enforcement, as evidenced by recent data:

To navigate the YA 2026 tax season without falling into the “Visibility Trap,” business owners must shift from reactive fixes to proactive governance.

Do not wait for an IRAS query to review your figures. Perform a rigorous internal audit of your 2025 payroll records before finalizing them in the myTax Portal. Key focus areas include:

Manual “shoebox accounting” remains the primary source of clerical errors. Migrating your financial records to a cloud-based digital system allows for real-time reconciliation. Accurate monthly records ensure that your year-end AIS submission is a verified reflection of your actual financial activity.

Tax compliance is intrinsically linked to corporate governance. Your Corporate Secretary ensures that all board resolutions-especially those regarding director compensation-are legally documented. Any discrepancy between secretarial records and tax filings is a major “red flag” that may lead IRAS to disallow tax-deductible expenses.

At Koobiz, we understand that tax compliance is not just about numbers; it’s about protecting your business’s reputation. Our integrated accounting and secretarial services ensure your AIS submissions are audit-ready long before the tax season begins. Let us turn the “Visibility Trap” into a benchmark of your corporate excellence. Contact Koobiz today for a Complimentary Tax Compliance & Payroll Health Check!

[SUMMARIES]

Every Singapore company must prepare four mandatory financial reports in strict compliance with SFRS standards.

Private firms qualify for audit exemption if they meet at least two of the ‘Small Company’ criteria, such as capping revenue or total assets at S$10 million.

Non-listed companies are required to hold an AGM within 6 months and file Annual Returns within 7 months of their financial year-end.

Most companies must file in the mandatory XBRL format to avoid ACRA enforcement actions and tiered fines.

Maintaining accurate financial records is a strategic necessity for measuring business performance and securing future funding.

[/SUMMARIES]

Running a business in Singapore requires navigating a robust regulatory landscape governed by ACRA and IRAS. However, maintaining accurate financial statements is more than just a matter of compliance – it is a strategic tool for unlocking your company’s growth potential. From the four essential types of reports to filing deadlines and step-by-step preparation, this guide provides everything you need to stay ahead.

A financial statement is a formal record that provides a structured overview of a company’s financial activities and performance over a specific period. In Singapore’s business environment, these statements are far more than mere documentation; they are vital for:

In short, an accurate financial statement is a non-negotiable asset for measuring success and ensuring your business remains in good standing.

Under the Singapore Financial Reporting Standards (SFRS), a complete set of financial statements provides a multi-dimensional view of a company’s financial health. To ensure statutory compliance and facilitate informed decision-making, directors and stakeholders rely on these four primary components:

The Balance Sheet provides a point-in-time snapshot of a company’s financial standing, typically at the end of the financial year (FYE). It details:

This statement summarizes revenues, costs, and expenses incurred over a specific reporting period. By deducting total expenses from total revenue, it reveals the net profit or loss. It is the primary tool for assessing a company’s operational efficiency and earnings sustainability.

While the income statement tracks profitability, the Cash Flow Statement tracks the actual inflow and outflow of cash. It categorizes movements into:

This document outlines the movements in a company’s equity over the reporting period. It reconciles the opening and closing balances by detailing:

To maintain its status as a leading global financial hub, Singapore enforces a strict, transparent, and internationally recognized accounting framework. All companies incorporated in Singapore are required to prepare their financial statements in accordance with these standards, which are regulated by the Accounting Standards Council (ASC).

The default accounting framework for businesses in Singapore is the SFRS. It is closely modeled after the International Financial Reporting Standards (IFRS), ensuring that financial statements prepared in Singapore are globally comparable, reliable, and transparent. Unless specifically exempted, all Singapore-registered companies must comply with SFRS when preparing their annual financial reports.

To reduce the administrative burden and compliance costs for smaller businesses, the ASC introduced the SFRS for Small Entities. This framework offers simplified reporting requirements. A company is eligible to adopt this standard if it meets at least two of the following three criteria for two consecutive financial years:

Adopting the SFRS for Small Entities is optional. Eligible companies can still choose to file under the full SFRS if preferred by their management or investors.

While SFRS is the mandatory domestic standard, the International Financial Reporting Standards (IFRS) may be applicable or preferred in specific corporate scenarios:

ACRA enforces strict reporting rules to uphold corporate transparency. Mastering these requirements is crucial to avoid severe penalties and streamline your annual filing process.

While every Singapore-incorporated company must prepare an annual financial statement, the rules for filing differ:

Statutory audits can be costly. Fortunately, private companies are audit-exempt if they qualify as a “Small Company” by meeting at least two of these three criteria for the past two consecutive financial years:

Note: Audit-exempt companies must still prepare an unaudited financial statement compliant with SFRS.

To facilitate digital data analysis, ACRA requires many companies to file statements in XBRL (eXtensible Business Reporting Language) format:

Timely submission is vital for maintaining your company’s “Good Standing” status. Delayed filings incur unnecessary costs and regulatory scrutiny.

Compliance timelines depend on your Financial Year End (FYE):

| Requirement | Non-Listed Companies | Listed Companies |

|---|---|---|

| Annual General Meeting (AGM) | Within 6 months post-FYE | Within 4 months post-FYE |

| Annual Return (AR) Filing | Within 7 months post-FYE | Within 5 months post-FYE |

Note: Financial statements must be approved at the AGM before AR filing with ACRA.

ACRA enforces strict penalties for late submissions. Directors are personally liable for ensuring statutory obligations are met.

A clean compliance record is essential for maintaining business reputation and accessing government grants or credit facilities.

Navigating the financial reporting process requires precision and a clear understanding of SFRS. Follow these six essential steps to ensure your company remains compliant.

Gather all supporting financial records for the financial year. This includes sales invoices, purchase receipts, bank statements, payroll records, and loan agreements. Organized documentation is the foundation of an accurate financial statement.

Enter all gathered data into your accounting system. Transactions must be categorized according to the Singapore Chart of Accounts. Ensure accruals, prepayments, and depreciation are properly adjusted to reflect the true financial position of the business.

Draft the four core components: the Balance Sheet, Profit and Loss Statement, Cash Flow Statement, and Statement of Changes in Equity. These must include necessary Notes to the Accounts, providing detailed breakdowns of specific line items as required by SFRS.

If your company does not meet the “Small Company” audit exemption criteria, you must appoint an independent Public Accountant registered with ACRA to audit your financial statements. The auditor will issue an opinion on whether the statements provide a “true and fair” view of the company’s finances.

Once finalized, financial data must be mapped and converted into XBRL format. Using ACRA’s BizFinx portal, this digital tagging ensures your data is compatible with regulatory analysis systems.

The final step involves two separate submissions:

To ensure seamless compliance and avoid ACRA investigations or tax penalties, directors should avoid these frequent pitfalls:

Choosing between in-house management and professional outsourcing is a strategic decision. Given Singapore’s complex regulatory environment, outsourcing is often the most efficient choice for SMEs and MNC subsidiaries.

Maintaining an internal team involves significant overheads, including salaries, training, and software costs. Furthermore, as SFRS and XBRL taxonomy evolve, in-house staff may struggle to maintain compliance, increasing the risk of errors and late-filing penalties.

Partnering with a professional firm offers distinct advantages:

At Koobiz, we provide expert accounting and filing services tailored to the Singapore corporate landscape. We ensure your financial statement is fully compliant with ACRA and IRAS, serving as a reliable roadmap for your business growth. Focus on your core operations and let Koobiz handle the complexities of compliance. Contact Koobiz today for a professional consultation and streamline your financial reporting.

[SUMMARIES]

Tax resident status in Singapore determines how individuals and companies are taxed and whether they can access key incentives under the IRAS tax framework.

Individuals generally qualify by meeting the 183-day rule or related administrative concessions, while companies must demonstrate that control and management are exercised in Singapore.

Tax residents benefit from progressive personal tax rates, corporate incentives such as SUTE and CIT rebates, and access to Singapore’s 90+ Double Taxation Agreements (DTAs).

They may also apply for a Certificate of Residence (COR) to claim treaty benefits in cross-border transactions.

Understanding these criteria and compliance requirements helps taxpayers optimize tax obligations and avoid common residency determination mistakes.

[/SUMMARIES]

Understanding the tax resident meaning in Singapore is essential for individuals and businesses operating in the country. Tax residency determines how income is taxed, the applicable tax rates, and whether taxpayers can access benefits such as tax exemptions and Double Taxation Agreements (DTAs). This guide explains the key residency criteria, benefits of tax resident status, and how individuals and companies can determine their tax status under the rules of the Inland Revenue Authority of Singapore.

In Singapore, the term “tax resident” refers to the tax status of individuals or companies that meet specific criteria relating to their physical presence or strategic management within the country during a given Year of Assessment (YA). This status determines how income is taxed and whether a taxpayer is eligible for certain tax incentives under Singapore’s tax system.

Tax residency in Singapore is administered by the Inland Revenue Authority of Singapore (IRAS). It is distinct from citizenship or permanent residency and is instead determined by practical factors such as the duration of stay in Singapore for individuals, or the location where a company’s control and management are exercised.

In Singapore, tax residency is not a uniform classification. IRAS applies different frameworks for individuals and companies, focusing on physical presence for individuals and strategic governance for corporate entities. Understanding these distinctions is important because tax residency determines applicable tax rates and eligibility for Singapore’s extensive network of tax treaties.

In Singapore, an individual is generally treated as a tax resident for a specific Year of Assessment (YA) if they stay or work in Singapore for at least 183 days in the preceding calendar year. Singapore citizens and Singapore Permanent Residents (SPR) who normally live in Singapore are also regarded as tax residents, except during temporary absences.

Foreign individuals may automatically qualify as tax residents if they hold a valid work pass for at least one year, in accordance with the rules of the Inland Revenue Authority of Singapore (IRAS).

IRAS also provides administrative concessions for longer work arrangements:

Tax residents are taxed under progressive personal income tax rates (0%–24%) and can claim personal tax reliefs, which often result in a lower effective tax burden compared with the flat tax rates (15%–24%) applied to non-residents.

For companies, tax residency is determined not by where the company is incorporated, but by where its control and management are exercised. This legal test focuses on the location where strategic business decisions are made rather than where day-to-day operations take place.

Key factors typically include:

A Singapore-incorporated company is not automatically considered a tax resident. It must demonstrate that its central management and strategic decision-making activities take place in Singapore to qualify for benefits such as the Start-Up Tax Exemption (SUTE) and relief under Double Taxation Agreements (DTAs).

Tax residency in Singapore provides access to a range of tax incentives and treaty benefits designed to support international businesses and professionals. For both individuals and companies, obtaining tax resident status can help optimize international tax obligations while benefiting from Singapore’s stable and business-friendly tax system.

Singapore maintains an extensive network of more than 90 Double Taxation Agreements (DTAs) with jurisdictions worldwide. These agreements help ensure that the same income is not taxed twice-once in the source country and again in Singapore.

Tax residents may claim benefits under these treaties, including reduced withholding tax rates on foreign-sourced dividends, interest, and royalties. These reduced rates, often ranging from 0% to 10%, are generally not available to non-resident taxpayers.

Singapore tax resident companies may benefit from residency-specific incentives such as the Start-Up Tax Exemption (SUTE), while all companies may receive Corporate Income Tax (CIT) rebates under Singapore Budget 2026.

Individual tax residents in Singapore are taxed under the progressive personal income tax system, with rates ranging from 0% to 24%, depending on income levels.

In contrast, non-resident individuals are typically subject to flat tax rates ranging from 15% to 24% on certain types of income. Additionally, tax residents may claim various personal tax reliefs, such as Earned Income Relief, Spouse Relief, and CPF Relief, which can significantly reduce the total tax payable.

Under the Foreign-Sourced Income Exemption (FSIE) scheme, Singapore tax resident companies may qualify for tax exemptions on certain foreign-sourced income remitted into Singapore, including:

To qualify, the income must generally have been taxed in the source country and the headline tax rate in that jurisdiction must be at least 15%.

Singapore tax residents may apply for a Certificate of Residence (COR) issued by the Inland Revenue Authority of Singapore (IRAS). This official document confirms that the taxpayer is a Singapore tax resident for a specific period.

The COR is commonly required when claiming tax treaty benefits under DTAs, particularly when dealing with foreign tax authorities or cross-border transactions.

Understanding tax residency status is essential for ensuring compliance and optimizing tax obligations. IRAS applies different tax treatments to residents and non-residents, particularly with respect to tax rates, relief eligibility, and corporate tax incentives for YA 2026.

| Feature | Tax Resident in Singapore | Non-Tax Resident in Singapore |

|---|---|---|

| Primary Criteria | Stay or work in Singapore ≥ 183 days; or company control and management exercised in Singapore | Stay or work in Singapore < 183 days; or strategic decisions made outside Singapore |

| Individual Tax Rates | Progressive tax rates (0% to 24%); first S$20,000 of income is tax-free | Employment income taxed at flat 15% or resident rate (whichever is higher) |

| Director’s Fees & Other Income | Taxed under progressive resident tax rates (0% to 24%) | Typically taxed at flat 24%, withheld at source |

| Tax Reliefs & Rebates | Eligible for various personal tax reliefs; no individual tax rebate for YA 2026 | Generally not eligible for personal tax reliefs or rebates |

| Corporate Benefits | May qualify for Start-Up Tax Exemption (SUTE) and 40% Corporate Income Tax Rebate (capped at S$30,000) + minimum S$1,500 Cash Grant (if the company had at least one local employee in 2025) | Eligible for 40% CIT Rebate (cap S$30,000) + minimum S$1,500 Cash Grant if the local employee (CPF) condition is met; generally not eligible for SUTE or Singapore DTA benefits |

| Treaty Benefits (DTA) | Access to Singapore’s 90+ Double Taxation Agreements | Generally not eligible to claim treaty benefits |

| Official Proof | May apply for a Certificate of Residence (COR) issued by IRAS | Not eligible to obtain a COR |

Important Note:For YA 2026, all companies (resident and non-resident) should note the revised 40% Corporate Income Tax (CIT) Rebate, capped at S$30,000. Although lower than the 50% rebate in the previous year, it remains a significant advantage compared with non-resident entities that do not qualify for such broad-based tax support.

A Certificate of Residence (COR) serves as official proof that an individual or company is a tax resident of Singapore. The certificate is issued by IRAS and is commonly required when claiming tax treaty benefits under Double Taxation Agreements.

Since 2025, IRAS has strengthened its economic substance requirements, making it increasingly important for companies to follow the correct application procedures through the myTax Portal.

Navigate to: e-Services → Corporate Tax (or Personal Tax) → Apply for Certificate of Residence (COR).

Applicants must provide:

Companies must confirm that strategic decisions are made in Singapore. IRAS may request supporting documents, including:

The standard processing time is typically 7 to 14 working days.

Once approved, applicants will receive a notification via email or SMS. The digital COR can then be downloaded directly from the portal.

IRAS has largely phased out physical paper certificates. The digital COR now includes a secure verification link or QR code, allowing foreign tax authorities to confirm the document’s authenticity online.

Misinterpreting Singapore’s residency rules can trigger higher tax liabilities and IRAS audits. Avoid these frequent pitfalls in 2026:

Determining tax residency in Singapore can be complex, particularly for companies with international directors or cross-border management structures. Koobiz Tax Advisory helps businesses navigate these rules and remain compliant with requirements set by the Inland Revenue Authority of Singapore.

Our Core Services:

By partnering with Koobiz, businesses can reduce the risk of non-resident taxation while ensuring efficient tax planning and full regulatory compliance.

[SUMMARIES]

Singapore donation tax relief allows businesses to claim a 250% tax deduction on qualifying donations made to approved Institutions of a Public Character (IPCs) under regulations administered by IRAS.

This incentive significantly reduces taxable income while encouraging corporate philanthropy and social impact.

Companies must distinguish between donations and sponsorships, as only voluntary contributions without commercial benefits qualify for enhanced deductions.

Eligible contributions may include cash, shares, property, artifacts, or volunteer expenses under the Corporate Volunteer Scheme (CVS).

When structured correctly and aligned with the Year of Assessment (YA), donation strategies can support corporate tax optimization, ESG goals, and regulatory compliance.

[/SUMMARIES]

Singapore offers attractive incentives for corporate giving through Singapore donation tax relief. Businesses that make qualifying charitable donations can claim up to a 250% tax deduction, reducing taxable income while supporting social causes. This guide explains how companies can benefit from donation tax relief, what donations qualify, and how to claim the deduction under the regulations of the Inland Revenue Authority of Singapore in Singapore.

Singapore donation tax relief allows companies to reduce their taxable income when making qualifying charitable contributions. Under regulations administered by the Inland Revenue Authority of Singapore (IRAS), businesses that donate to approved charities may claim enhanced tax deductions, helping reduce their overall corporate tax liability.

In most cases, donations made to organizations with Institution of a Public Character (IPC) status qualify for a 250% tax deduction. This means companies can deduct 2.5 times the donated amount from their taxable income. The incentive encourages corporate giving while supporting a wide range of social causes across Singapore.

Singapore offers one of the most generous tax incentives for charitable giving in Asia. Under regulations administered by the Inland Revenue Authority of Singapore (IRAS), companies making qualifying donations to approved Institutions of a Public Character (IPCs) are entitled to a 250% tax deduction on the donated amount.

For example, if your company donates SGD 10,000, it can deduct SGD 25,000 from its taxable income. This enhanced deduction significantly lowers your company’s taxable profit, making philanthropy a highly effective tool for both corporate tax planning and social impact.

As announced in Budget 2026, the 250% tax deduction for qualifying donations to approved IPCs has been officially extended until 31 December 2029, giving businesses greater long-term certainty for strategic philanthropy and tax planning.

A common pitfall for businesses is misclassifying contributions, which may lead to potential audit issues with IRAS. The key distinction lies in whether the company receives commercial benefits in return.

| Criteria | Donation | Sponsorship |

|---|---|---|

| Definition | A voluntary contribution made to an approved IPC without expecting commercial benefits. | A payment made in exchange for promotional or marketing benefits. |

| Commercial Benefit | No material benefit is received. A simple acknowledgment (e.g., donor name listed in a report) is generally acceptable. | The company receives benefits such as advertising, event exposure, or marketing rights. |

| Tax Treatment | Eligible for 250% tax deduction under Singapore donation tax relief. | Treated as a business or marketing expense. |

| Deduction Amount | 250% of the donation amount can be deducted from taxable income. | 100% of the payment can be deducted as a business expense. |

To qualify for Singapore donation tax relief, corporate contributions must comply with the guidelines established by the Inland Revenue Authority of Singapore (IRAS). In general, for a deduction to be valid, the donation must be made to an approved Institution of a Public Character (IPC) or through government-recognized schemes.

Below are the primary forms of corporate giving that qualify for tax incentives.

This is the most common form of corporate giving. Contributions made via bank transfer, PayNow (Corporate), or cheque to registered IPCs are eligible for the 250% tax deduction, provided the donor does not receive any material benefit in return.

Donating immovable property, such as land or buildings, to an IPC is considered a significant philanthropic contribution. The deductible amount is determined based on the market valuation conducted by a professional valuer and remains subject to approval by IRAS.

Under the Public Gallery Tax Incentive Scheme, businesses that donate heritage artifacts or artworks to museums with IPC status may claim tax deductions. The items must be evaluated by the National Heritage Board (NHB) to confirm their cultural or historical significance.

When a company makes a substantial contribution that allows a building, facility, or scholarship to be named after the donor, it may still qualify as a donation rather than a sponsorship, provided the naming does not involve commercial advertising or product promotion.

Under the Overseas Humanitarian Assistance Tax Deduction Scheme (OHAS), Singapore companies may claim a 100% tax deduction on qualifying cash donations made for overseas humanitarian emergencies through designated charities. This pilot scheme is valid until 31 December 2028.

Qualifying deductions under OHAS are subject to an overall cap of 40% of statutory income, which applies specifically to overseas donation schemes as administered by the Inland Revenue Authority of Singapore.

To remain compliant, businesses must distinguish between a genuine charitable donation and a commercial transaction. According to guidelines issued by the Inland Revenue Authority of Singapore (IRAS), the following contributions are not eligible for the 250% tax deduction.

Only donations made to registered Institutions of a Public Character (IPCs) qualify for tax relief. The following contributions are not eligible:

Payments that provide commercial benefits are not considered charitable donations. Examples include:

These payments are typically treated as business or marketing expenses, not tax-deductible donations.

Donations that involve conditions or personal benefits may also be disqualified. For example:

To qualify for tax relief, the contribution must be a voluntary donation with no expectation of personal or commercial gain.

One of the key benefits of Singapore’s donation tax incentive is the 250% tax deduction, which can significantly reduce a company’s taxable income. This policy, administered by the Inland Revenue Authority of Singapore, allows businesses in Singapore to combine corporate philanthropy with tax efficiency.

Example calculation:

Revised taxable income:

Corporate tax impact (17% rate):

Summary:

| Item | Amount |

|---|---|

| Donation Amount | SGD 10,000 |

| Tax Deduction (250%) | SGD 25,000 |

| Tax Saved (17%) | SGD 4,250 |

This example shows how a qualifying corporate donation not only supports charitable initiatives but also helps companies optimize their corporate tax liability when structured correctly.

Integrating Singapore donation tax relief into a company’s financial strategy allows businesses to support social causes while improving tax efficiency. By planning the timing and structure of donations, companies can maximize the 250% tax deduction and remain compliant with the Inland Revenue Authority of Singapore regulations.

To claim the deduction in the upcoming Year of Assessment (YA), donations must be made within the current financial year. Companies with higher profits often donate before financial year-end to reduce taxable income and optimize corporate tax payable.

In Singapore, corporate tax follows a preceding year basis, meaning the YA reflects income from the previous financial year.

To ensure the deduction is applied correctly:

If your company’s approved donation deductions exceed its statutory income for a given Year of Assessment (YA), the unutilized portion may be carried forward for up to five subsequent YAs to offset future taxable income.

To qualify for this carry-forward treatment, the company must satisfy the shareholding test, meaning there must be no substantial change (50% or more) in its ultimate shareholders and their respective shareholdings during the relevant period.

Important note: Unlike unutilized trade losses or capital allowances, donation deductions cannot be carried back to offset income from previous Years of Assessment under the Loss Carry-Back Relief scheme, as clarified by IRAS.

Previously known as the Business and IPC Partnership Scheme (BIPS), the Corporate Volunteer Scheme (CVS) allows businesses to claim Singapore donation tax relief through employee volunteer services instead of direct cash donations.

Supported by the Inland Revenue Authority of Singapore in Singapore, the scheme encourages companies to support approved Institutions of a Public Character (IPCs) by providing skilled or general volunteer services.

Under CVS, companies can claim a 250% tax deduction on qualifying expenses incurred when employees volunteer at IPCs.

Eligible expenses include:

Key Limitations for Strategic Planning:

To maintain tax efficiency, companies should note the following caps:

By leveraging CVS, businesses can strengthen corporate social responsibility (CSR), improve employee engagement, and contribute professional expertise to community initiatives-while still benefiting from Singapore’s enhanced tax deduction framework.

In today’s business landscape, corporate giving has evolved beyond simple philanthropy; it is now a core component of a robust Environmental, Social, and Governance (ESG) framework. By strategically leveraging Singapore donation tax relief, businesses can drive meaningful social change while fulfilling their Corporate Social Responsibility (CSR) mandates.

For companies operating in Singapore, integrating charitable giving into their ESG strategy offers several strategic advantages:

When charitable giving is woven into the corporate DNA, the 250% tax deduction acts as a catalyst, allowing businesses to amplify their impact while maintaining fiscal discipline and responsible governance.

Claiming Singapore donation tax relief is relatively simple thanks to the digital integration between approved charities and the Inland Revenue Authority of Singapore (IRAS).

In most cases, the process is fully automated. Approved Institutions of a Public Character (IPCs) are required to submit donation records electronically to IRAS. As a result, the 250% tax deduction is typically pre-filled when companies file their corporate income tax return (Form C-S or Form C).

To ensure a smooth claim and maintain compliance, businesses should follow these best practices:

Following these steps helps companies claim the tax deduction efficiently while remaining fully compliant with Singapore’s corporate tax regulations.

Although Singapore donation tax relief offers attractive tax benefits, some companies make mistakes that prevent them from claiming the 250% tax deduction properly. To remain compliant with the Inland Revenue Authority of Singapore in Singapore, businesses should avoid the following common errors:

Avoiding these mistakes helps businesses maximize tax benefits while maintaining full compliance with Singapore’s tax regulations.

Although Singapore donation tax relief offers strong tax benefits, compliance and tax planning can be complex. Businesses must ensure donations qualify for the 250% tax deduction, align with the correct YA, and meet the requirements of the Inland Revenue Authority of Singapore in Singapore.

Many companies therefore work with professional advisors to:

At Koobiz Corporate Services, businesses receive expert support in corporate tax planning, compliance, and donation tax relief strategies, helping maximize tax efficiency while integrating charitable giving into broader tax and ESG strategies.

[SUMMARIES]

Two Primary Paths: A Singapore company can be closed through Striking Off (fast and low-cost for dormant companies) or Winding Up (a formal liquidation process for complex or insolvent cases).

Solvency is Key: Directors must determine if the company can pay all debts (solvent) or not (insolvent) to choose the correct legal path.

Tax Verification: Singapore does not issue a physical “Tax Clearance Letter” for company strike-offs. Directors must ensure all tax matters are fully settled and confirm there are no outstanding issues via the IRAS myTax Portal.

Director Liability: Improper company closure can expose directors to fines, enforcement actions, or even director disqualification under the Companies Act.

Professional Help: Appointing an experienced corporate secretary such as Koobiz helps ensure full compliance with the Companies Act and reduces the risk of objections that could delay or block the closure process.

[/SUMMARIES]

Deciding to cease business operations in Singapore requires careful legal and regulatory planning to avoid penalties and director exposure. Knowing how to close a Singapore company correctly is crucial. At Koobiz, we simplify the complex ACRA and IRAS regulations for directors. This guide compares Striking Off vs. Winding Up, helping directors choose the correct exit strategy in compliance with ACRA and IRAS requirements.

")

Closing a company in Singapore is the formal legal process of terminating a business entity’s existence and removing it from the Official Register maintained by ACRA. This process ensures all corporate matters are properly settled, assets are distributed, and the company permanently ceases to exist as a legal entity.

To avoid penalties, directors must understand the difference between simply stopping work and a legal exit:

Important: Until a company is formally struck off or wound up, ACRA continues to treat it as an active entity. Directors who ignore ongoing obligations because “business has stopped” often face avoidable fines and court summonses.

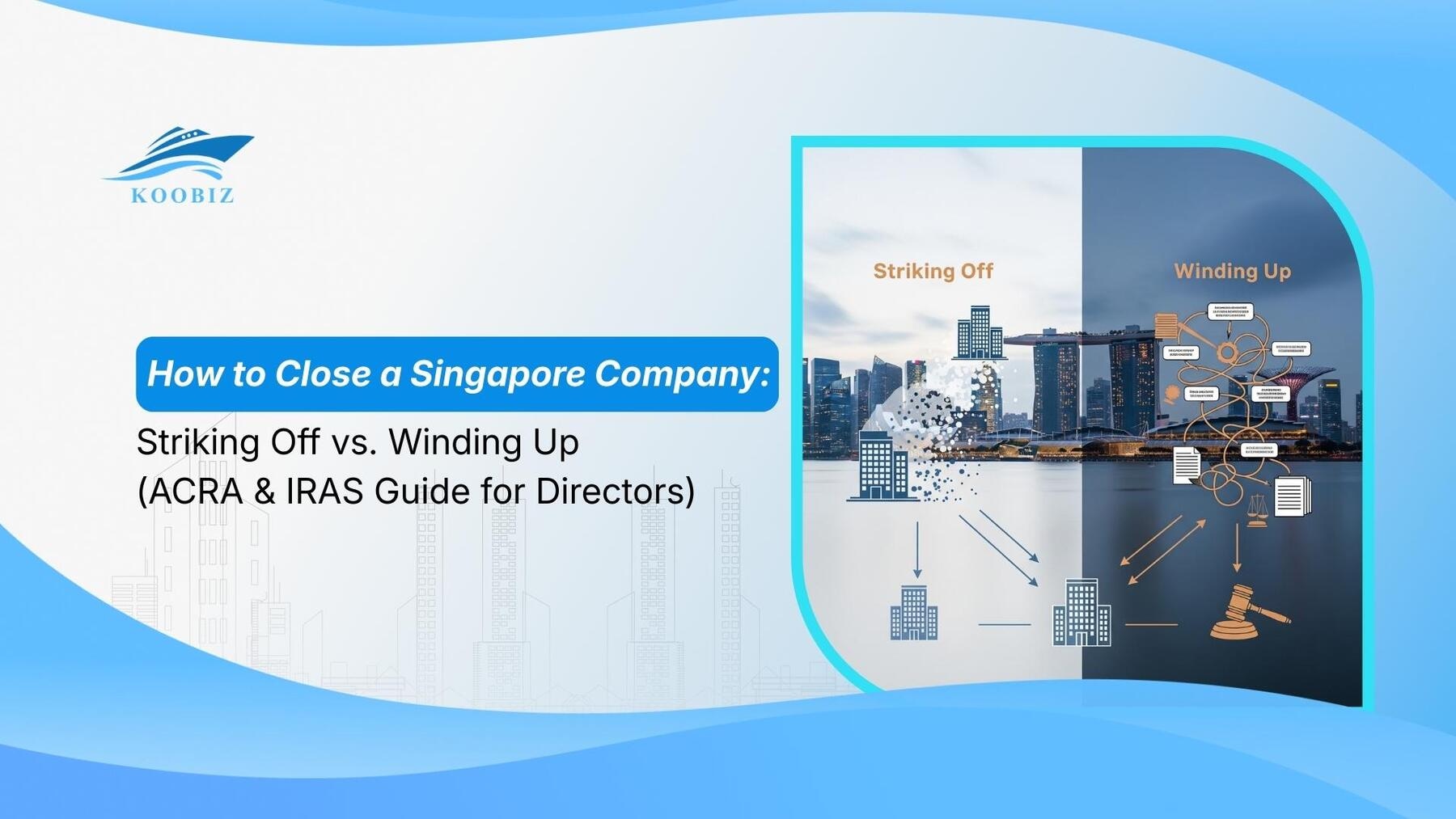

There are two legally recognised methods to close a Singapore company: Striking Off and Winding Up. The appropriate path depends on the company’s financial position and operational status.

To determine which option applies to your situation, directors can follow the decision logic below:

Striking off is the administrative process of removing a company’s name from the official register maintained by ACRA, and is suitable for dormant companies with a clean compliance record. Although commonly described as a fast-track process, directors should note that statutory timelines still apply. In practice, striking off typically takes around four to six months to protect creditors’ interests.

Before reviewing the timeline, directors must ensure the company meets the eligibility criteria imposed by ACRA. If you fail any of these, the application will be rejected or objected to:

To manage expectations, the striking-off process can be divided into four statutory stages.While the application itself is quick, the statutory waiting periods are mandatory.

Stage 1: Preparation & Tax Verification (Month 0–1)

This is the most critical phase, as ACRA may reject the application if the company’s records are not fully in order.

Stage 2: The Application (Week 1)

Once the company’s records are fully compliant, the formal application can be submitted.

Stage 3: The Gazette Period (Month 2–4)

This is a mandatory statutory waiting period designed to protect creditors and the public.

Stage 4: Final Dissolution (Month 5–6)

While striking off is an administrative process, Winding Up (Liquidation) is a formal legal procedure for terminating a company. This route is mandatory if your company still holds assets that need distributing or has debts it cannot settle immediately.

Unlike striking off, Winding Up involves appointing a licensed Liquidator who takes control of the company’s affairs to ensure a fair distribution of resources.

The winding-up process splits into two distinct paths based on one critical question: Is your company Solvent?

Who this applies to: Companies that are profitable or asset-rich but no longer have a commercial purpose (e.g. director retirement or group restructuring).

In an MVL, the directors formally declare that the company is solvent, meaning it is able to pay all its debts in full within 12 months.

Who this applies to: Companies facing financial distress and unable to pay debts as they fall due.

In a CVL, the company is insolvent and unable to meet its financial obligations. The directors cannot sign a Declaration of Solvency because the company’s liabilities exceed its assets.

Striking Off is generally more cost-effective and faster, while Winding Up provides a formal legal resolution for complex or insolvency cases. To help directors at Koobiz clients make an informed choice, we have summarized the key differences below.

| Feature | Striking Off | Winding Up (Liquidation) |

|---|---|---|

| Primary Use Case | Dormant companies with no assets and no liabilities. | Active companies with assets, liabilities, or insolvency. |

| Cost | Low to none (Government fees + Secretarial fees) | High (liquidator fees and statutory filing costs). |

| Timeframe | Approx. 4–6 months. | 12 months or longer (depending on complexity). |

| Solvency | Must have Zero assets and liabilities. | Can be Solvent (MVL) or Insolvent (CVL). |

| Process Owner | Directors / Corporate Secretary. | Licensed Liquidator. |

| Director Control | High (Directors manage the process). | None/Low (Liquidator takes legal control). |

| Risk of Restoration | Higher (can be restored within 6 years). | Lower (Dissolution is generally final). |

Table: Comparison of Company Closure Methods in Singapore

Many directors mistakenly believe that ceasing business operations automatically ends tax obligations. This is incorrect. ACRA will reject a striking-off application if IRAS has not cleared the company’s tax position.

To ensure a successful application, the company must be in a fully compliant clean status with no outstanding regulatory or tax issues.

It is a common misconception that IRAS issues a physical tax clearance letter for striking off. This is not true. Instead, tax “clearance” is confirmed through self-verification on the IRAS myTax Portal. You must log in to the IRAS myTax Portal and confirm that:

If you apply to ACRA while tax matters are pending, IRAS will lodge an objection, halting your application.

Use this checklist to ensure you are ready before our team submits your application:

Koobiz Pro Tip: Always verify directly via the IRAS myTax Portal that the Statement of Accounts shows a zero balance before instructing a strike-off filing.

Directors have a strict fiduciary duty to ensure the company’s affairs are handled honestly during the closing process. ACRA and the courts take a serious view of directors who use closing procedures to evade debts.

WARNING: The Solvency Trap

Making a Declaration of Solvency in an MVL without reasonable grounds is a criminal offence. If the company later proves insolvent, directors may face fines of up to S$10,000, imprisonment of up to 12 months, or both. Under the Insolvency, Restructuring and Dissolution Act (IRDA), penalties may escalate if fraudulent intent is proven.

Generally, a company is a separate legal entity. However, in closing scenarios, the law can “pierce the corporate veil,” making directors personally liable for company debts if:

Your job isn’t done when the company closes. Under the Companies Act, directors must retain all company books and records for at least five years from the date of dissolution.

Conclusion

Closing one business chapter is often a necessary step before starting the next.While ensuring your company is closed compliantly is vital to avoid liability, your focus should be on what comes next.

At Koobiz, we understand that entrepreneurship is a cycle. We are not just here to help you exit; we are your strategic partner for your next venture. As an established corporate services provider, Koobiz specialises in:

Whether you are closing a dormant entity to restructure or planning your next big idea, Koobiz provides the foundation for your business success.

Disclaimer: This guide is for informational purposes only and does not constitute legal advice. Laws and regulations regarding company closure in Singapore (including ACRA and IRAS fees) are subject to change. Please consult with a qualified professional or corporate secretary for advice specific to your situation.

[SUMMARIES]

Legal Requirement: Salary withholding is required under the Income Tax Act and is not a discretionary decision made by your employer.

Travel Freedom: You generally can leave Singapore while the process is ongoing, provided you have no outstanding tax debts triggering a Stop Payment Order.

Timeline: Withheld salary is typically released within 7 days for e-filing or up to 21 days for paper filing after your employer submits Form IR21.

Self-Check: You can verify if your tax clearance is complete by logging into the myTax Portal using your personal SingPass.

Residency Impact: Your final tax liability depends on the 183-day rule, which determines whether you are taxed as a Resident (progressive rates of 0–22%) or a Non-Resident (flat 15%).

[/SUMMARIES]

Seeing a “zero” balance on your final payslip due to tax withholding can be stressful, especially for foreign employees preparing to leave Singapore. Are you stuck in Singapore? At Koobiz, we understand that for foreign employees, Tax Clearance (Form IR21) is more than just paperwork—it directly affects your final salary and departure plans. This guide explains Singapore’s mandatory tax withholding rules, the expected timeline for releasing your salary, and how to track your tax clearance status via myTax Portal—so you can leave Singapore compliantly and with peace of mind.

It’s a stressful moment: you’re packing up your life, bills are due, and suddenly your final paycheck is frozen. It feels personal, but in reality, it isn’t.

Your employer is complying with the Singapore Income Tax Act, specifically Section 68(5). This law requires employers to withhold all payments—salary, bonuses, overtime, and leave encashment—when a foreign employee resigns or leaves Singapore.

The Logic: Since you are leaving the country, IRAS needs a guarantee that your final tax bill will be paid. Your withheld salary serves as a form of security for your final tax assessment If your employer releases the money to you and you leave without paying tax, they become legally liable to pay your tax debt. Because of this strict legal liability, HR departments generally have no discretion to make exceptions.

Under IRAS regulations, employers who fail to file Form IR21 or properly withhold salary may face a fine of up to SGD 1,000 or imprisonment of up to six months. This explains why your request for an early release of funds is almost always denied.

Whether you can leave Singapore depends on your tax clearance status. Below are the most common scenarios:

Scenario A: Form IR21 Filed, Money Withheld

Scenario B: Tax Bill Issued, Shortfall Paid

Scenario C: Outstanding Tax Debt or Suspected Non-Compliance

The release of withheld salary follows a clear timeline involving three key stages: resignation, IRAS processing, and the issuance of the Clearance Directive. Understanding this flow is essential for managing your cash flow, especially if you need funds for relocation costs or flight tickets.

Here is the typical chronological breakdown:

In an ideal e-filing scenario, you can typically expect to receive your remaining salary about one week after your employer submits the form. If you are leaving in a rush, asking your employer to e-file is the single most effective way to speed up your payment.

You don’t need to wait for HR to email you. You can track the progress of your tax clearance directly through the IRAS system. This is the fastest way to know when your money is ready to be released.

Prerequisite: You must have a valid SingPass.

Note: If you cancel your Employment Pass (EP), your SingPass remains active only while you hold a valid immigration pass (such as the Short-Term Visit Pass issued upon cancellation). This is typically valid for 30 days (standard) to 90 days (maximum, if approved). It is advisable to log in as soon as possible to verify your contact details before your access expires.

The 3-Step Check:

Pro Tip: Once the Clearance Directive appears in your myTax Portal, the same directive will also have been issued to your employer. Sharing a screenshot with your HR or payroll team can help prompt the timely release of your remaining salary.

The Clearance Directive will result in one of two outcomes. Check your Directive to see which applies to you:

| Outcome | What it Means | Action Required |

|---|---|---|

| Scenario A: SHORTFALL

(Tax Due > Withheld) |

You owe more tax than your employer held back. | PAY IMMEDIATELY.

Use the Payment Slip to pay via Internet Banking/AXS. Failure to pay risks a travel ban. |

| Scenario B: REFUND

(Tax Due < Withheld) |

You overpaid (via withholding). The employer owes you the balance. | WAIT FOR EMPLOYER.

Your employer will release the remaining funds to your bank account. No action needed with IRAS. |

While the standard procedure applies to most, many foreign employees face unique circumstances. While the standard process applies to most cases, foreign employees often encounter specific edge cases. Being aware of these scenarios can help prevent unnecessary tax exposure, delays, and administrative complications.

Situation 1: The “183-Day” Residency Trap

Situation 2: Permanent Residents (SPR) Changing Jobs Without Leaving Singapore (LOU)

Situation 3: Refunds after Bank Closure

Leaving Singapore marks the close of an important chapter, and tax clearance is often the final administrative step before you move on. While salary withholding can be frustrating, it is a standard legal requirement rather than a punitive measure. By understanding the clearance timeline, actively tracking your status through the myTax Portal, and being aware of how residency rules affect your final tax bill, you can manage the process with greater certainty and avoid unnecessary delays.

At Koobiz, we specialize in simplifying business and financial compliance in Singapore. While this guide focuses on the employee’s perspective, we also assist companies in managing their employer obligations, from accurate Form IR21 filing to corporate tax planning and accounting. If you are a business owner or HR manager needing assistance with tax clearance procedures or general corporate compliance, visit Koobiz.com to see how our expert team can support your operations.